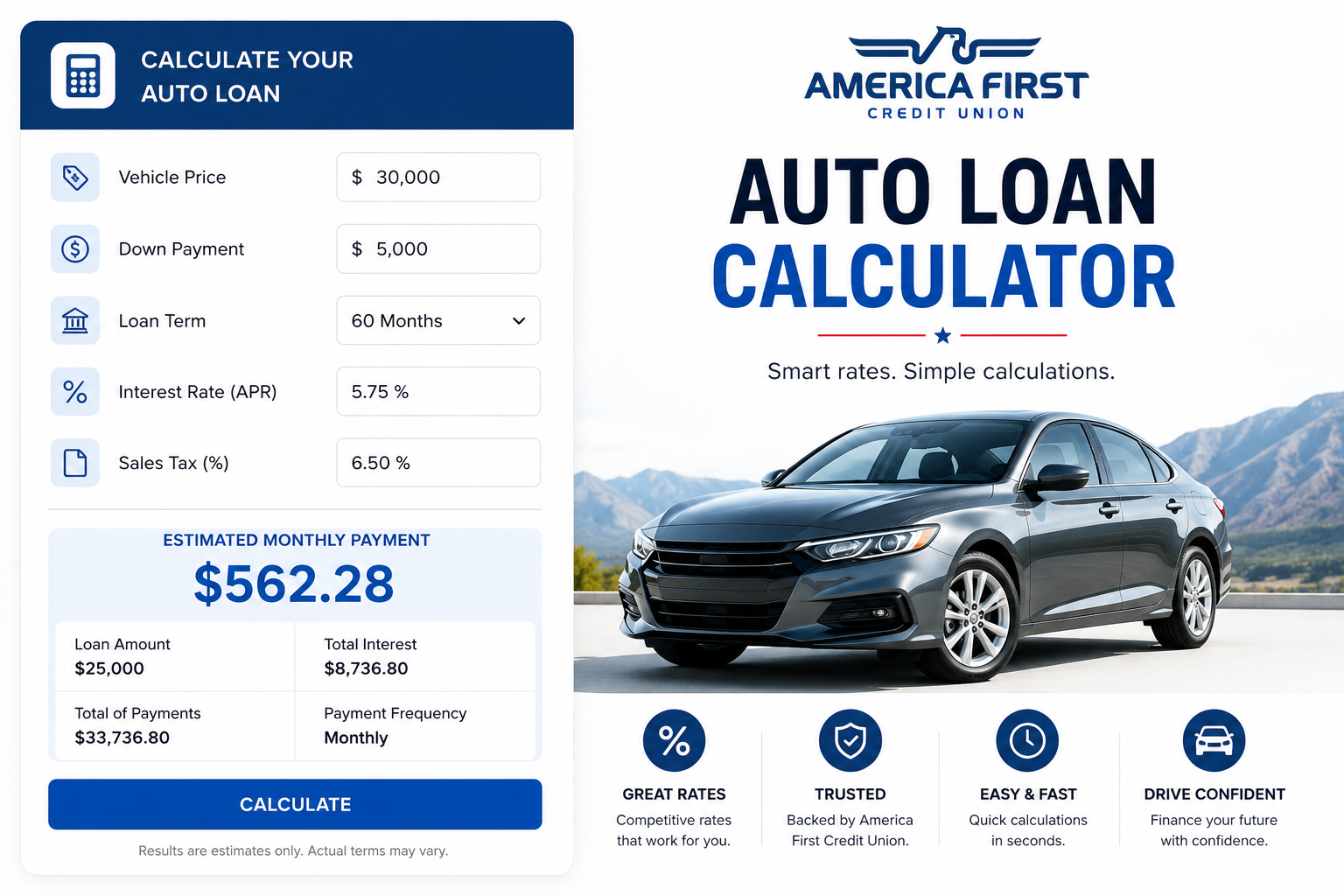

This is an independent, general-purpose auto loan calculator — it estimates your monthly payment, full amortization schedule, and refinance savings for any auto loan, regardless of which bank or credit union you finance with. It is not affiliated with, endorsed by, or officially connected to America First Credit Union or any other specific lender. If you’re a America First Credit Union member (or considering becoming one), use this tool to model the numbers, then confirm your actual rate and terms directly with America First Credit Union, since real rates depend on your credit profile, the vehicle, and current market conditions.

Use the Monthly Payment tab to estimate your payment and total interest, the Amortization Schedule tab to see your balance decline year by year, or the Refinance Comparison tab to see whether refinancing your current auto loan would save you money — instantly.

Table of Contents

- Auto Loan Calculator (Free Tool)

- How Auto Loan Payments Are Calculated

- What Affects Your Auto Loan Rate

- Credit Union Auto Loans vs. Bank and Dealer Financing

- Using the Amortization Schedule to Plan Extra Payments

- Should You Refinance Your Auto Loan?

- How to Get an Accurate Rate Quote

- Frequently Asked Questions

Auto Loan Calculator

Select a tab below to estimate your monthly payment, view a full amortization schedule, or compare refinancing your current loan. All fields are editable — enter your own numbers or a quote from your lender for an accurate result.

| Year | Remaining Balance | Principal Paid (Year) | Interest Paid (Year) |

|---|

How Auto Loan Payments Are Calculated

Every standard auto loan uses the same amortization formula, regardless of which bank, credit union, or dealer finance company you use:

Monthly Payment = P × r ÷ (1 − (1 + r)⁻ⁿ), where P is the amount financed, r is your monthly interest rate (APR ÷ 12), and n is the number of monthly payments (loan term in months).

Each payment is split between interest (calculated on your current remaining balance) and principal (which reduces that balance) — early in the loan, more of each payment goes to interest since the balance is still high; later, more goes to principal as the balance shrinks. Use the Amortization Schedule tab above to see this split play out year by year for your specific loan.

What Affects Your Auto Loan Rate

- Credit score: The single biggest factor in most cases — borrowers with stronger credit histories typically qualify for meaningfully lower rates than those with limited or weaker credit.

- New vs. used vehicle: New vehicle loans commonly carry lower rates than used vehicle loans, partly reflecting the lender’s risk assessment on an asset that depreciates differently.

- Loan term: Shorter terms often come with somewhat lower rates than longer terms, in addition to accumulating less total interest simply by virtue of being shorter.

- Loan-to-value ratio: A larger down payment or trade-in reduces the amount financed relative to the vehicle’s value, which can improve your rate and approval odds.

- Membership and relationship discounts: Many credit unions offer a modest rate discount for existing members, automatic payment setup, or bundling with other accounts — ask any credit union you’re considering, including America First Credit Union, what discounts you may qualify for.

Credit Union Auto Loans vs. Bank and Dealer Financing

Credit unions are member-owned, not-for-profit financial institutions, and as a general category they’re often able to offer more competitive auto loan rates than traditional banks or dealer-arranged financing, since they’re not working to generate profit for outside shareholders. This is a general industry pattern, not a guarantee for any specific institution or borrower — actual rates always depend on your individual credit profile and the specific lender’s current pricing.

Dealer-arranged financing can be convenient (approval happens on the spot, at the point of sale) but often includes a markup over the wholesale rate the dealer receives from the actual lending institution — it’s frequently worth comparing a pre-approved rate from your own bank or credit union, such as America First Credit Union or any other institution you’re a member of, against what the dealer offers before signing, since you’re free to finance a dealer purchase through an outside lender in most cases.

Using the Amortization Schedule to Plan Extra Payments

The amortization schedule isn’t just a curiosity — it’s a planning tool. Because early payments carry a higher proportion of interest, any extra principal payment made earlier in the loan term saves more total interest than the same extra payment made later, when less balance (and therefore less interest) remains outstanding. If you’re considering paying extra toward your auto loan, front-loading those extra payments — rather than spreading them evenly or waiting until later in the term — generally produces the largest interest savings for the same total extra dollars paid.

Should You Refinance Your Auto Loan?

Refinancing replaces your current auto loan with a new one — ideally at a lower rate, though the full picture depends on both the rate and the term:

- Your credit has improved since your original loan: If your credit score has risen meaningfully since you financed the vehicle, you may now qualify for a noticeably better rate than you originally received.

- Rates in general have dropped: Broader interest rate movements can make refinancing worthwhile even without a personal credit change.

- You want a lower monthly payment: Extending the term can lower your payment, but — as the Refinance Comparison tab above demonstrates — this can increase total interest paid even at a lower rate, so weigh payment relief against total cost deliberately, not just the monthly number.

- You’re not near the end of your loan or underwater on the vehicle: Refinancing tends to make the least sense very close to your existing loan’s payoff date, or if you owe significantly more than the vehicle is currently worth.

Many credit unions, including America First Credit Union, offer auto loan refinancing as a standard product — if you’re considering it, request a current rate quote directly and run it through the Refinance Comparison tab above against your existing loan’s actual numbers.

How to Get an Accurate Rate Quote

This calculator estimates payments off whatever rate and term you enter — it doesn’t know, and can’t predict, what rate any specific lender will actually offer you. To get an accurate number to plug in:

- Check your current credit standing before applying, since your score is one of the biggest rate drivers.

- Get pre-qualified or pre-approved with your bank or credit union — many, including America First Credit Union, offer this without a hard credit inquiry.

- Compare at least two or three offers — your own bank or credit union, a competing institution, and the dealer’s financing — since rates and terms genuinely vary between lenders for the same borrower.

- Ask about membership or relationship discounts specifically, since many are not applied automatically and require you to ask or enroll in autopay.

Frequently Asked Questions

Is this calculator affiliated with America First Credit Union?

No. This is an independent, general-purpose auto loan calculator, not affiliated with, endorsed by, or officially connected to America First Credit Union or any other specific financial institution. It works the same regardless of which lender you’re financing with — simply enter the rate and terms you have or are considering.

Where do I find America First Credit Union’s current auto loan rates?

Rates change regularly and depend on your credit profile, the vehicle, and the loan term, so the only reliable source is America First Credit Union directly — through their website, a branch, or a loan officer. Once you have a quoted rate, enter it into the Monthly Payment or Amortization Schedule tab above to see the resulting payment and full cost breakdown.

Does a lower monthly payment always mean a better loan?

No. A lower payment often comes from a longer loan term, which can mean paying more total interest over the life of the loan even at the same or a lower rate. Always compare both the monthly payment and the total interest cost — the Refinance Comparison tab above is built specifically to show both side by side.

Should sales tax and fees be included in the “vehicle price” field?

Only if you’re financing them. Many buyers roll sales tax, title, and registration fees into the total amount financed rather than paying them separately at signing — if that’s your plan, add those costs to the vehicle price field so the calculator reflects your true financed amount and resulting payment.

Is it worth refinancing to a shorter term instead of a longer one?

A shorter term generally raises your monthly payment but reduces total interest paid, since less time is spent accruing interest on the remaining balance. Whether that trade-off is worth it depends on your budget — the Refinance Comparison tab above lets you test different new-loan terms against your current loan to see the exact trade-off in your own numbers.