Leasing an Audi gives you access to a new luxury vehicle every two to three years — with lower monthly payments than financing and coverage under the factory warranty for the entire lease term. But the numbers behind an Audi lease are more complex than a simple car loan. Your payment depends on the vehicle’s MSRP, the negotiated selling price (cap cost), the residual value set by Audi Financial Services (AFS), the money factor (lease interest rate), and the term. Our free Audi Lease Calculator puts all of those variables together so you can estimate your exact monthly payment, compare lease terms side by side, and run a buy vs. lease cost analysis — all before you walk into the dealership.

Use the Payment tab to calculate a monthly lease payment with a full cost breakdown, the Compare Terms tab to see 24-, 36-, and 48-month leases side by side, or the Buy vs. Lease tab to analyze the true total cost of each option.

Table of Contents

- Audi Lease Calculator (Free Tool)

- How an Audi Lease Payment Is Calculated

- Understanding Money Factor — The Hidden Lease Interest Rate

- Residual Value by Audi Model — What to Expect

- What You Can Negotiate on an Audi Lease

- Audi Financial Services Fees Explained

- Tips for Getting the Best Audi Lease Deal

- Frequently Asked Questions

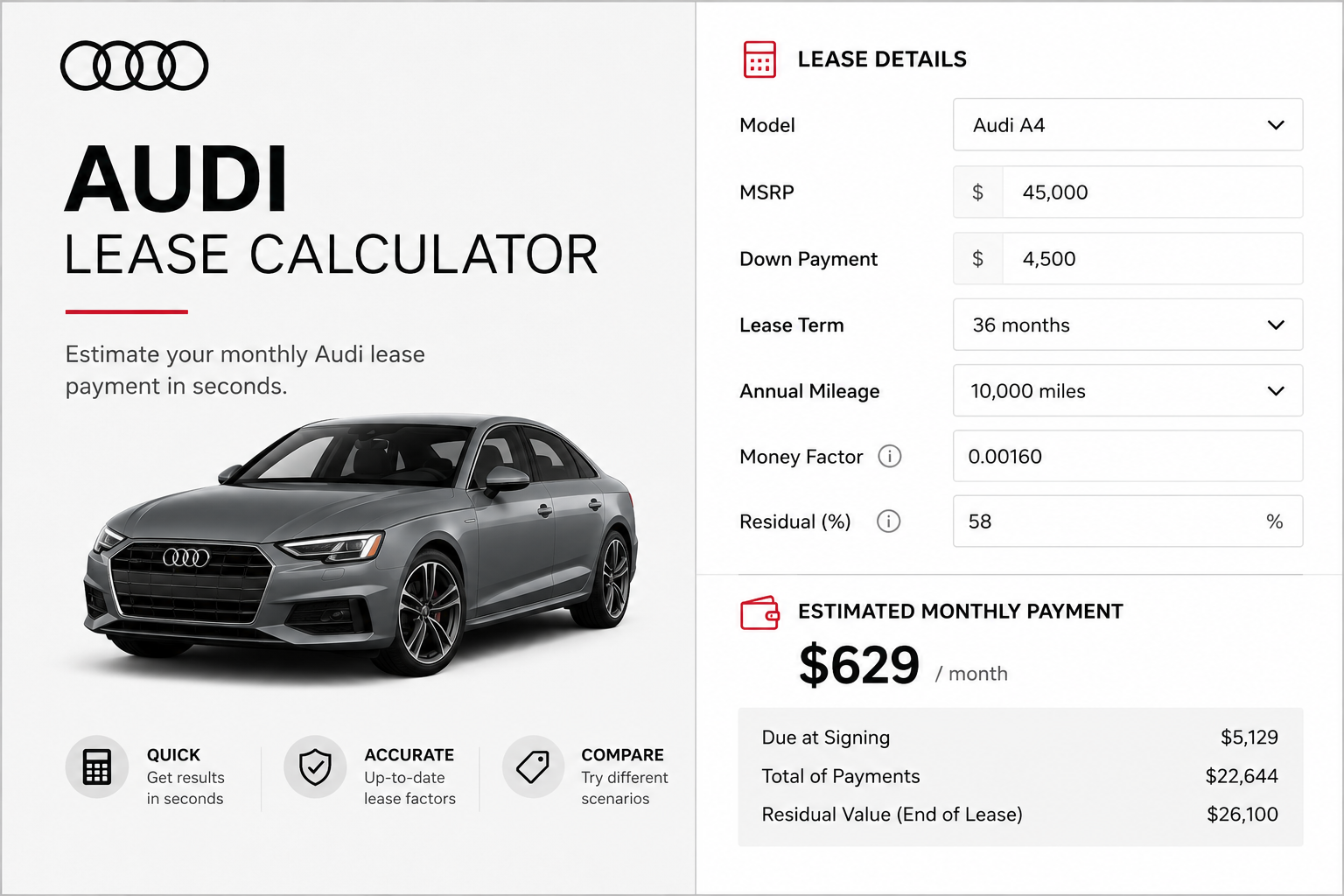

Audi Lease Calculator

The calculator is pre-loaded with values typical of a new Audi Q5. Enter your vehicle’s MSRP and the terms from your dealer’s offer — including the money factor and residual percentage provided by Audi Financial Services — to get an instant payment estimate.

How an Audi Lease Payment Is Calculated

An Audi lease payment is made up of two core components added together each month: a depreciation fee and a finance charge. Unlike a loan payment, which pays down principal and interest, a lease payment covers only the portion of the vehicle’s value you consume during the lease term — plus the cost of financing that depreciation.

Understanding Money Factor — The Hidden Lease Interest Rate

The money factor (MF) is how Audi Financial Services expresses the interest rate on a lease. It looks like a tiny decimal — typically something like 0.00125 — which makes it easy for dealerships to obscure the true cost of financing. To convert a money factor to its approximate annual percentage rate (APR), simply multiply by 2,400:

Dealers are legally allowed to mark up the money factor above the “buy rate” set by AFS — and the markup goes directly into the dealer’s pocket. Always ask the dealer: “What is the buy rate money factor for this vehicle this month?” If they refuse to disclose it, that is a red flag. Websites like LeasHackr and Edmunds publish monthly money factor and residual data for most Audi models, giving you a benchmark before you walk in.

Residual Value by Audi Model — What to Expect

The residual value is the single most powerful factor in determining your monthly payment — more impactful than the money factor in most cases. Audi Financial Services sets residual values monthly and they vary by model, trim, term, and mileage tier. The table below shows typical residual value ranges to help you benchmark — always get the current figure from your dealer.

| Audi Model | Typical 36-Mo Residual | 12k mi/yr Adj. | Leaseability |

|---|---|---|---|

| A3 / A3 Sedan | 48–54% | −1–2% vs 10k | Moderate |

| A4 Sedan | 50–56% | −1–2% vs 10k | Good |

| A5 / S5 Coupe | 49–55% | −1–2% vs 10k | Good |

| A6 Sedan | 47–53% | −1–2% vs 10k | Moderate |

| Q3 | 50–56% | −1–2% vs 10k | Good |

| Q5 / Q5 Sportback | 52–58% | −1–2% vs 10k | Best |

| Q7 | 48–54% | −1–2% vs 10k | Good |

| Q8 / SQ8 | 46–52% | −1–2% vs 10k | Moderate |

| e-tron / Q8 e-tron | 38–48% | −1–3% vs 10k | Lower |

| e-tron GT | 40–50% | −1–3% vs 10k | Variable |

Residual values are set monthly by Audi Financial Services and vary by trim, options, and region. The above are historical ranges for planning reference only — confirm current values with your dealer.

The Q5 consistently holds among the highest residual values in Audi’s lineup, making it the most lease-friendly model. Electric models (e-tron family) historically carry lower residuals due to uncertainty in EV resale markets — though this can change quickly when AFS runs subsidized lease programs to move inventory.

What You Can and Cannot Negotiate on an Audi Lease

You CAN Negotiate

- Selling price / capitalized cost

- Cap cost reduction (down payment)

- Money factor (ask for buy rate — refuse markups)

- Dealer add-ons and accessories

- Pre-paid maintenance packages

- Mileage allowance (buy extra miles upfront cheaply)

- Disposition fee waiver (if re-leasing an Audi)

You CANNOT Negotiate

- Residual value (set by AFS, not dealer)

- Acquisition fee (set by AFS)

- Base money factor / buy rate (set by AFS)

- Excess mileage penalty rate

- Wear-and-tear standards

- Lease-end purchase price (= residual)

Audi Financial Services Fees Explained

| Fee | Typical Amount | Notes |

|---|---|---|

| Acquisition Fee | ~$895 | Charged by AFS to initiate the lease. Can be rolled into the cap cost (increases monthly payment) or paid at signing. |

| Disposition Fee | ~$395 | Charged at lease end if you return the vehicle and don’t re-lease or purchase from Audi. Often waived for loyalty customers re-leasing a new Audi. |

| Security Deposit | $0 (waived) | Audi Financial Services typically does not require a security deposit for well-qualified lessees. |

| Excess Mileage Fee | ~$0.25/mile | Charged per mile over the contracted annual allowance at lease end. Pre-purchasing miles at signing is usually cheaper. |

| Excess Wear & Tear | Varies | Charges for damage beyond “normal wear” as assessed at lease return. Audi offers a wear care protection program through dealers. |

| Early Termination Fee | Significant | Ending a lease early is very costly. You typically owe the remaining payments plus fees. Avoid unless absolutely necessary. |

| Registration / Tax | Varies by state | Sales tax on lease payments varies by state. Some states (e.g., TX) tax the full vehicle value upfront; most tax each monthly payment. |

Tips for Getting the Best Audi Lease Deal

- Negotiate the selling price before discussing the lease. The capitalized cost (selling price) is the single number you have the most control over, and lowering it reduces both your depreciation fee and your finance charge simultaneously. Treat it like a cash purchase negotiation first.

- Always ask for the buy rate money factor. Dealers may mark up the AFS buy rate by 0.0005 to 0.002 — which sounds tiny but translates to hundreds of dollars over the lease term. Ask explicitly: “What is the buy rate money factor for this vehicle this month?” and compare it to published data on Edmunds or LeasHackr.

- Time your lease to coincide with Audi incentive programs. AFS runs subsidized “event” lease rates on specific models at the end of each model year, during major auto shows (January, April), and around holidays. These specials include reduced money factors and/or boosted residuals that can significantly cut your payment.

- Target the Q5 for leasing. Among all Audi models, the Q5 consistently offers the most lease-friendly combination of high residual value and available incentive programs. If you are open to different Audi models, the Q5 almost always produces the lowest payment relative to MSRP.

- Put as little money down as possible. In a lease, any down payment (cap cost reduction) is lost immediately if the vehicle is totaled — insurance pays AFS the residual value, not you. Keep cap cost reduction low and put that money in a savings account to cover your first few months of payments instead.

- Get a loyalty waiver on the disposition fee. If you plan to stay in an Audi, ask the dealer to document that the $395 disposition fee will be waived when you return the current vehicle and sign on a new one. This is standard policy at most Audi dealers for returning AFS customers.

- Use our calculator before every negotiation session. Enter the dealer’s numbers — MSRP, selling price, money factor, residual — into the calculator above and verify their quoted payment matches the formula. If the quoted payment is higher than your calculation, you are being marked up somewhere.

Frequently Asked Questions

How is an Audi lease payment calculated?

An Audi lease payment equals the monthly depreciation fee plus the monthly finance charge, multiplied by applicable sales tax. The depreciation fee is the adjusted capitalized cost minus the residual value, divided by the number of months. The finance charge is the sum of the adjusted cap cost and residual value, multiplied by the money factor. The adjusted cap cost is the negotiated selling price plus the acquisition fee, minus any cap cost reduction (down payment, trade-in, or rebates). Use the Payment tab in our calculator above to see this broken down line by line.

What is a good money factor for an Audi lease?

A “good” money factor depends on current market conditions and your credit tier. As a general benchmark: a money factor equivalent to a sub-4% APR (i.e., MF below 0.00167) is considered competitive for a luxury lease. A money factor equivalent to 2–3% APR (MF 0.00083–0.00125) represents an excellent, often incentivized rate. To convert any money factor to APR, multiply by 2,400. Always verify the current AFS buy rate for your specific model and month — do not accept a dealer markup without pushing back.

Can I negotiate the residual value on an Audi lease?

No — the residual value is set by Audi Financial Services, not the dealership, and it is non-negotiable. This is actually a protection for you as a consumer: a higher AFS residual directly reduces your monthly payment, and no dealer can manipulate it to extract profit. What you can negotiate is the selling price (cap cost), which interacts with both the depreciation fee and the finance charge. Lowering the selling price has roughly the same effect as a higher residual.

What happens if I go over my mileage on an Audi lease?

If you exceed your contracted annual mileage allowance at lease end, Audi Financial Services charges a per-mile overage fee — typically $0.25 per mile, as specified in your lease contract. For example, if you drive 2,000 miles over your allowance on a 36-month lease, you owe $500 at turn-in. To avoid this, you can pre-purchase additional miles at signing (usually at a lower per-mile rate than the penalty) if you know you drive more than the standard allowance. Use the Mileage Overage section in the Payment tab above to estimate your exposure.

Is it better to put money down on an Audi lease?

In most cases, no — minimize your down payment on a lease. Any capitalized cost reduction you make is not refundable if the vehicle is stolen or totaled early in the lease — the insurance company pays the AFS residual value, and your down payment is gone. Instead, keep your cap cost reduction as low as possible and use that money to cover the first few months of payments from a savings account. The only time a larger cap cost reduction makes sense is if the resulting monthly payment is the absolute deciding factor in your budget approval.

Can I buy my Audi at the end of the lease?

Yes — at lease end, you have the option to purchase the vehicle for the pre-determined residual value specified in your contract, plus applicable taxes and fees. If the vehicle’s current market value (what it would sell for as a used car) exceeds the residual value, buying out the lease gives you an immediate equity gain — essentially purchasing the car below market price. You can finance the buyout through AFS or any other lender. The disposition fee is typically waived if you purchase the vehicle rather than returning it.

Which Audi model has the best lease deals?

The Audi Q5 consistently offers the best lease value in the lineup due to its combination of high residual value, frequent AFS promotional money factors, and strong demand. The Q3 offers excellent value for those seeking a lower-MSRP entry point into the Audi lease ecosystem. The A4 is the best sedan lease value. Avoid leasing electric models (e-tron) unless AFS is running a subsidized incentive program with a boosted residual, as standard e-tron residuals tend to be lower due to EV market uncertainty.

What credit score do I need to lease an Audi?

Audi Financial Services generally requires a credit score of 700 or higher to qualify for standard lease programs and the best advertised money factors. Scores of 720–740+ typically qualify for Tier 1 (best) rates. Applicants with scores between 650–699 may still qualify but at higher money factors and less favorable terms. Below 650, AFS approval becomes unlikely, and you may need to explore other financing sources or improve your credit profile before applying. Keep in mind that the quoted lease deals in Audi advertisements almost always require Tier 1 credit qualification.