“Bi-monthly” is one of the most genuinely ambiguous words in English — dictionaries list it as meaning both “every two months” and “twice a month,” and people use it both ways constantly. This calculator covers both interpretations so you get the right math regardless of which one you meant: pay every 2 months (6 payments a year), pay twice a month (24 payments a year), or compare every common car payment frequency side by side to see which one actually saves you money.

Use the Every 2 Months tab if you want to pay less often in larger chunks, the Twice a Month tab if you want to split your payment across two paychecks, or the Compare All Frequencies tab to see monthly, semi-monthly, bi-weekly, and every-2-months side by side — instantly.

Table of Contents

- Bi-Monthly Car Payment Calculator (Free Tool)

- What Does “Bi-Monthly” Actually Mean?

- Paying Every 2 Months: How It Works

- Paying Twice a Month: How It Works

- Which Payment Frequency Actually Pays Off Your Loan Faster?

- Always Confirm How Your Lender Applies Off-Cycle Payments

- Frequently Asked Questions

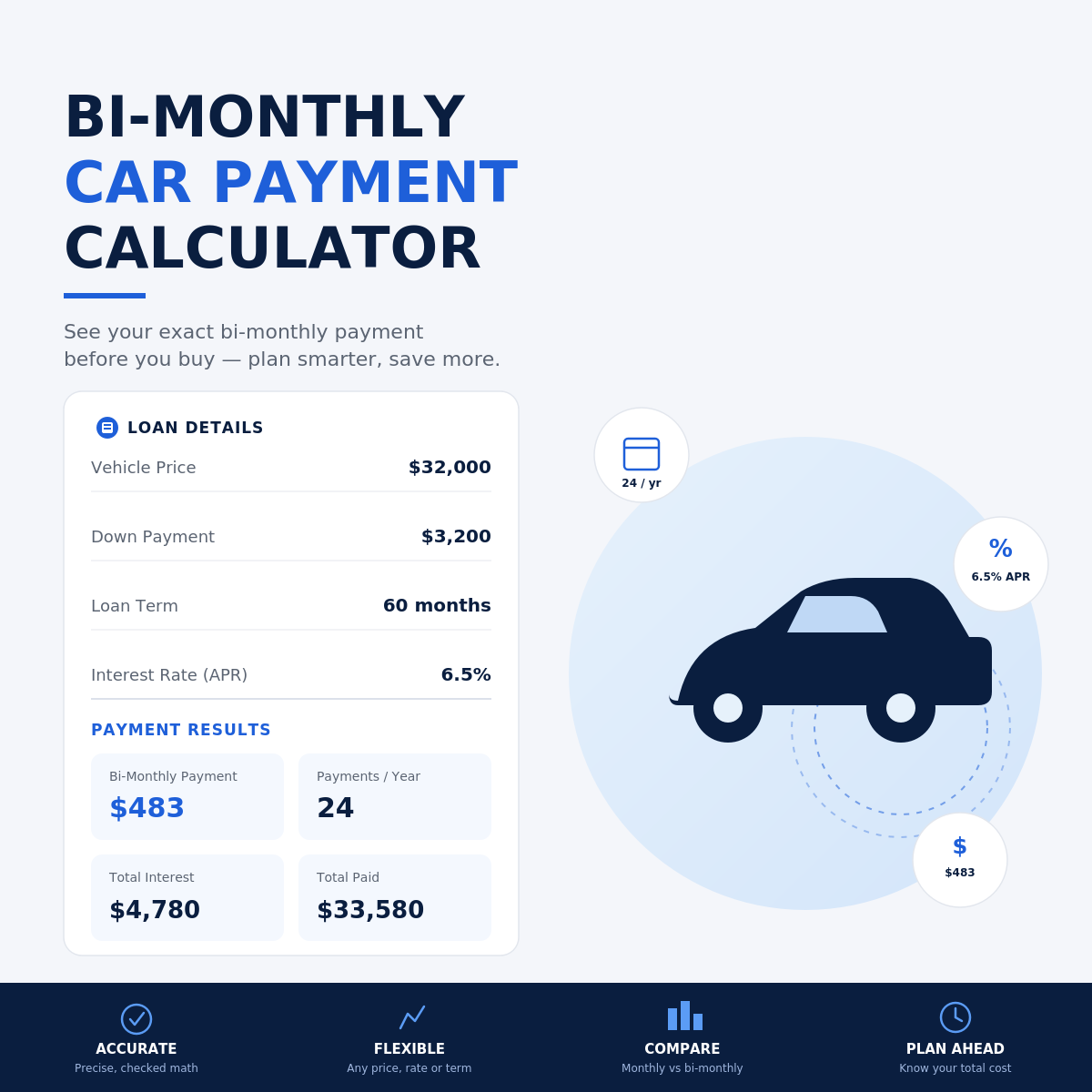

Bi-Monthly Car Payment Calculator

Select a tab below based on which “bi-monthly” you mean, or use the comparison tab if you’re not sure which schedule is actually best for you.

| Schedule | Payment Amount | Payments/Year | Payoff Time | Total Interest |

|---|

What Does “Bi-Monthly” Actually Mean?

“Bi-monthly” is a genuinely ambiguous word, and this isn’t a case of people simply using it wrong — major dictionaries list both meanings as valid: (1) occurring every two months, and (2) occurring twice a month. Both usages are common in everyday speech, which means when someone says “bi-monthly car payment,” they could mean a large payment every other month, or a smaller payment split across two paydays each month.

Because the two interpretations produce completely different payment amounts and schedules, this calculator covers both directly rather than guessing which one you meant.

Paying Every 2 Months: How It Works

Paying every 2 months means 6 payments a year instead of 12. To keep pace with a standard loan, each payment needs to be roughly double your normal monthly payment — some people prefer this if their income arrives in larger, less frequent chunks (certain commission structures, seasonal work, or simply a personal budgeting preference for fewer, bigger transactions rather than many small ones).

Mathematically, paying exactly 2× your standard monthly payment every 2 months produces essentially the same payoff timeline and total interest as paying monthly — the total amount paid per year is identical, just delivered in a different rhythm. The Every 2 Months tab above lets you test any payment amount, including one larger than 2× your standard payment if you want to actually accelerate payoff.

Paying Twice a Month: How It Works

Paying twice a month means 24 payments a year — often appealing because it lines up naturally with a semi-monthly paycheck (paid on, say, the 1st and 15th). Splitting your standard monthly payment in half and paying it twice a month produces essentially the same payoff timeline and total interest as paying the full amount once a month, since 24 half-payments equal exactly 12 full payments across the year.

This is worth understanding clearly if you’re comparing “bi-monthly” (twice a month) against true bi-weekly payments (every 14 days, 26 times a year) — the two sound similar but aren’t mathematically equivalent. Bi-weekly adds one extra half-payment’s worth of money to the year (26 vs. 24), which is what actually accelerates payoff; twice-a-month payments, on their own, do not.

Which Payment Frequency Actually Pays Off Your Loan Faster?

Of the common car payment schedules, only true bi-weekly (a fixed payment every 14 days, regardless of the calendar) genuinely accelerates payoff on its own, because it works out to 13 full monthly payments per year instead of 12. Monthly, twice-a-month, and every-2-months schedules are all mathematically equivalent to each other when scaled proportionally — same total annual payment, same payoff time, same total interest, just delivered on a different rhythm.

The real lever for paying off any car loan faster isn’t the payment frequency — it’s paying more money per year than the loan requires, whether that comes from choosing true bi-weekly, adding a fixed extra amount to any schedule, or simply making one extra lump-sum payment whenever you have the cash. Use the Compare All Frequencies tab above to see this side by side with your own loan numbers.

Always Confirm How Your Lender Applies Off-Cycle Payments

Whichever schedule you choose, the math above only holds if your lender applies each payment to your balance as it’s received. Some loan servicers instead hold non-standard payments (anything off the original monthly due date) in a suspense or holding account until a full scheduled payment amount has accumulated, then apply it on the regular due date — which erases any benefit from paying more frequently, since your money isn’t reducing principal any sooner than it would have anyway. Before committing to any off-cycle payment plan, ask your lender directly whether payments are applied to principal immediately upon receipt.

Frequently Asked Questions

Does “bi-monthly” mean every 2 months or twice a month?

Both — dictionaries recognize both meanings as valid, and everyday usage genuinely splits between them. There’s no universally agreed-upon single meaning, which is exactly why this calculator covers both interpretations separately rather than assuming one.

Is a bi-monthly car payment cheaper than a monthly one?

Not inherently — under either definition of “bi-monthly,” a proportionally-scaled payment (2× monthly if paid every 2 months, or half of monthly if paid twice a month) produces essentially the same total interest as paying monthly. The payment frequency itself doesn’t create savings; paying more total money per year than the loan requires does.

Is bi-monthly the same as bi-weekly?

No, and they’re commonly confused. Bi-weekly typically means every 14 days (26 payments/year), which is one extra payment’s worth more than 24 twice-a-month payments — that extra amount is what actually accelerates a bi-weekly schedule’s payoff. “Bi-monthly” in either of its meanings (every 2 months or twice a month) doesn’t have this same acceleration effect on its own.

Will my lender let me pay every 2 months or twice a month?

Most auto loan servicers accept payments whenever you choose to make them through their standard online payment portal, as long as your account stays current by the actual due date on your loan agreement. Confirm with your specific lender whether off-cycle payments are applied to principal immediately, since some servicers hold non-standard payments until a full scheduled payment has accumulated.

What’s the best way to actually pay off my car loan faster?

Pay more total money per year than the loan strictly requires — through true bi-weekly payments, a fixed extra amount added to any schedule, or occasional lump-sum extra payments — rather than simply changing how often you make the same total annual payment. Frequency alone, under most common “bi-monthly” interpretations, doesn’t accelerate payoff; extra money does.