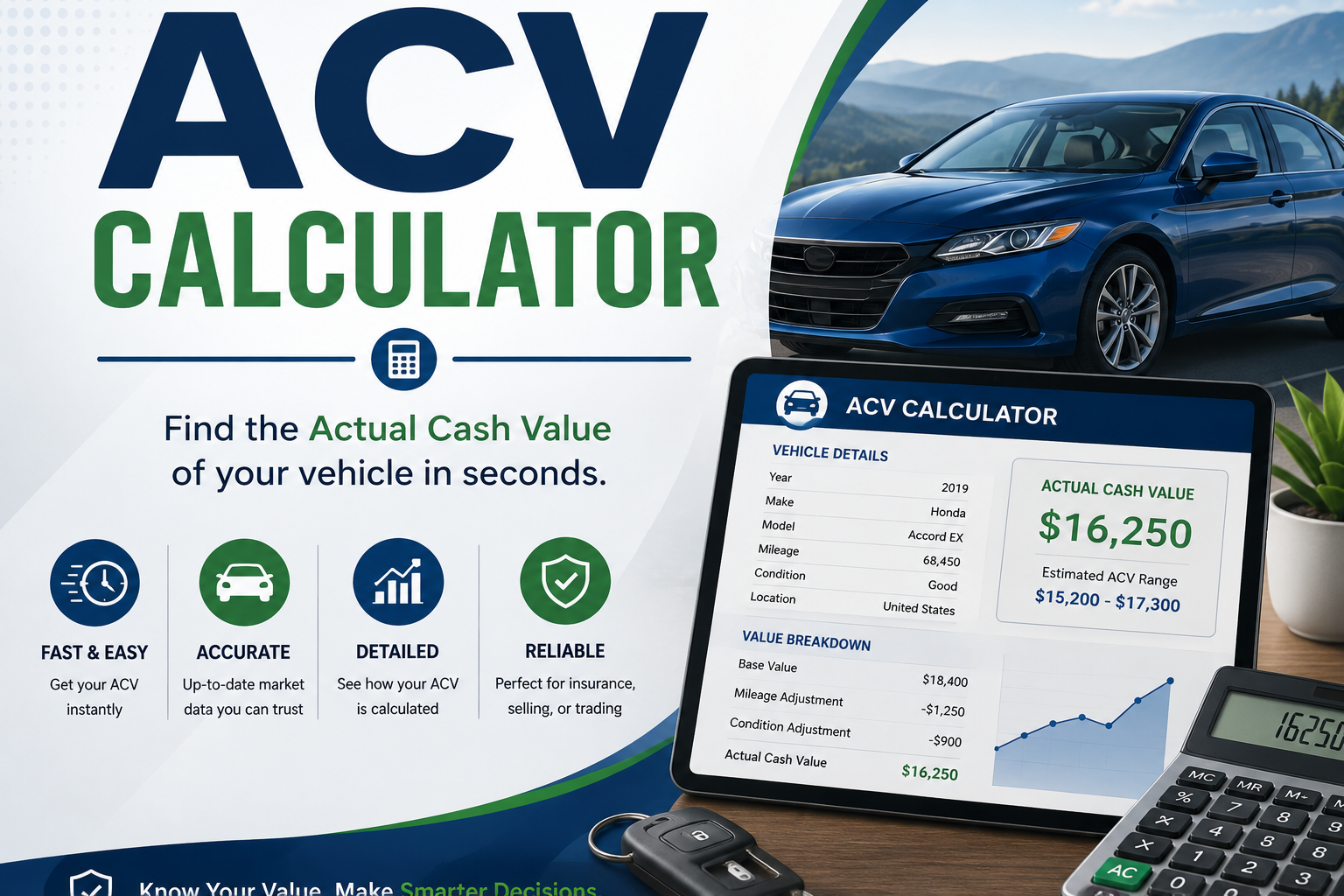

The ACV Calculator — Actual Cash Value — helps you estimate what your car is really worth today, not what you paid for it. Insurance companies use ACV to determine your payout after a total loss claim, and understanding how that number is built gives you the leverage to spot a lowball offer before you sign off on it. This tool covers three angles: estimating your car’s current ACV, calculating your likely total loss settlement, and viewing a full year-by-year depreciation schedule.

Use the ACV Estimator tab to calculate your vehicle’s current actual cash value, the Total Loss Payout tab to estimate what an insurer would actually cut you a check for, or the Depreciation Schedule tab to see how your car’s value declines year by year — instantly.

Table of Contents

- ACV Calculator (Free Tool)

- What Is Actual Cash Value (ACV)?

- How Is ACV Calculated for a Car?

- ACV vs. Replacement Cost vs. Trade-In Value

- How a Total Loss Insurance Payout Works

- Factors That Increase or Decrease Your Car’s ACV

- How to Dispute a Low ACV Offer

- Frequently Asked Questions

🚗 ACV Calculator — Actual Cash Value for Cars

Select a tab below to estimate your car’s actual cash value, calculate a total loss settlement, or generate a full depreciation schedule. All fields can be adjusted to your vehicle and local currency.

| Year | Estimated Value | Annual Depreciation | % of Original Retained |

|---|

What Is Actual Cash Value (ACV)?

Actual Cash Value (ACV) is the estimated dollar value of your car at the moment right before it was damaged, stolen, or declared a total loss — not what you paid for it, and not what it would cost to buy an identical new one today. Insurers define ACV as replacement cost minus depreciation: what a similar used vehicle, of the same make, model, year, mileage, and condition, would sell for in your local market right now.

ACV matters most in two situations: when your car is declared a total loss after an accident (repair costs exceed a set percentage of the car’s value, typically 70–80% depending on the state), or when it’s stolen and not recovered. In both cases, your insurer isn’t paying to replace your car with a brand-new one — they’re paying you what your specific car was worth the day before the loss occurred.

This is different from Replacement Cost Value (RCV) coverage, which some specialty policies offer and which pays to replace your vehicle with a new equivalent regardless of depreciation. Most standard auto insurance policies use ACV, which is why understanding how it’s calculated — and how to challenge a number that seems too low — is worth a few minutes of your time.

How Is ACV Calculated for a Car?

Insurers typically start with a market-based valuation report — pulling comparable local sale prices from databases like CCC ONE, Mitchell WorkCenter, or Audatex — then adjust for your specific vehicle’s condition. This calculator approximates that process using a transparent depreciation model so you can sanity-check any number an adjuster gives you:

ACV = Base Depreciated Value × Mileage Adjustment × Condition Adjustment × Title/History Adjustment

1. Base Depreciated Value (Age)

New cars lose value fastest in the first year — commonly 15–25% the moment it’s driven off the lot and through year one. This calculator models it as 20% in year one, 15% per year through year five, and 10% per year after that, compounding — meaning each year’s loss is calculated against the already-reduced value, not the original price. A $28,000 car following this curve is worth roughly $16,000–$17,000 at 4 years old before any mileage or condition adjustment.

2. Mileage Adjustment

Average annual mileage is commonly benchmarked at 12,000 miles/year. A car with significantly more mileage than expected for its age is adjusted downward; one with less is adjusted upward. This calculator applies roughly 1% per 1,000 miles of deviation from the expected mileage, capped at ±15%, which reflects how most valuation tools weight this factor.

3. Condition Adjustment

Condition is graded against a baseline of “good” (normal wear, mechanically sound, regularly maintained). Excellent condition can add roughly +10%; fair condition with visible wear or needed repairs subtracts roughly 10%; poor condition with mechanical issues can subtract 20% or more.

4. Title & Accident History Adjustment

A clean title with no reported accidents holds full value. A vehicle with a professionally repaired, reported accident typically loses 5–15% of its value even after quality repairs — this is often called “diminished value.” A salvage or rebuilt title is the most severe hit, frequently cutting value by 30–50% or more, since many buyers and lenders avoid salvage-titled vehicles entirely.

ACV vs. Replacement Cost vs. Trade-In Value

These three numbers are frequently confused, but they answer different questions and are calculated differently:

- Actual Cash Value (ACV): What your specific used car was worth immediately before a covered loss, based on depreciation and market comparables. Used by insurers for total loss and theft claims under standard policies.

- Replacement Cost Value (RCV): What it would cost to buy a brand-new equivalent vehicle today, with no depreciation subtracted. Only available on specialty “new car replacement” or “gap”-adjacent endorsements — rare in standard auto policies and usually limited to the first 1–2 years of ownership.

- Trade-In Value: What a dealership would offer to take your car off your hands as part of a new purchase. Trade-in value is typically lower than ACV or private-sale market value because the dealer needs margin to recondition and resell the car at a profit.

- Private Party / Market Value: What you could realistically sell the car for yourself, without a dealer’s margin. This is usually the closest real-world comparison to a well-calculated ACV — and the figure most worth comparing your insurer’s offer against.

If your insurer’s ACV offer looks closer to a trade-in number than a private-party number, that’s often your first sign the offer is too low.

How a Total Loss Insurance Payout Works

When an insurer declares your vehicle a total loss, the payout isn’t simply the ACV figure — several adjustments apply on top of it:

- Start with ACV: The insurer’s determination of your car’s pre-loss market value.

- Add sales tax and fees (where applicable): Many states require insurers to reimburse the sales tax and title/registration fees you’d pay to replace the vehicle — this is often missed unless you ask for it explicitly.

- Subtract your deductible: Whatever deductible applies to the coverage (collision or comprehensive) that’s paying the claim.

- Subtract any loan payoff shortfall (if you have a loan): If you owe more on your auto loan than the ACV payout, you’ll need gap insurance to cover the difference — otherwise you owe the shortfall out of pocket. The Total Loss Payout tab above does not include loan payoff; check your own loan balance separately.

- Subtract salvage value (if you keep the vehicle): You can often keep the totaled car in exchange for a salvage title, but the insurer deducts the car’s salvage/scrap value from your payout.

Use the Total Loss Payout tab above to model your specific numbers — plugging in your ACV, deductible, local sales tax rate, and any fees to see a realistic net payout estimate.

Factors That Increase or Decrease Your Car’s ACV

Factors That Increase ACV

- Low mileage relative to age: Below-average miles for the car’s age signals less mechanical wear and directly raises comparable-sale value.

- Documented maintenance history: Full service records demonstrate the car was cared for, which adjusters and buyers both value.

- Desirable trim, color, or options package: Popular configurations (all-wheel drive, sought-after colors, higher trims) sell faster and for more in the comparable-sales data insurers pull from.

- Recent major repairs or new tires: Recently replaced tires, brakes, or a new battery can be itemized and added back to an ACV offer if you provide receipts.

- Clean, single-owner history: Vehicle history reports (Carfax/AutoCheck) showing one owner and no accidents support a higher valuation.

Factors That Decrease ACV

- High mileage for the vehicle’s age: The single biggest downward adjustment in most valuation reports.

- Prior accidents, even repaired ones: “Diminished value” persists even after quality bodywork, because vehicle history reports disclose the accident to future buyers.

- Salvage or rebuilt title: Severely limits the buyer pool and financing options, cutting value sharply.

- Mechanical issues or needed repairs: Anything a buyer would need to fix themselves gets subtracted, often at retail repair-cost estimates.

- Aftermarket modifications: Non-factory modifications (unless professionally documented and desirable) are frequently valued at $0 by insurers, or even viewed as a negative.

- Cosmetic damage unrelated to the claim: Pre-existing dents, stains, or wear beyond normal use reduce the comparable condition grade.

How to Dispute a Low ACV Offer

If your insurer’s ACV offer feels low, you have real leverage to push back — insurers expect some negotiation and most valuation reports have an appeals process built in.

- Request the full valuation report: Ask your adjuster for the comparable vehicles used to calculate your ACV. You’re entitled to see this in most states.

- Check the comparables yourself: Look up similar vehicles (same year, trim, mileage range) for sale within roughly 100–150 miles on sites like Autotrader, Cars.com, and CarGurus. If your comparables consistently sell for more than the insurer’s figure, you have documentation to push back with.

- Submit condition and maintenance documentation: Service records, recent repair or tire receipts, and photos of the vehicle’s condition before the loss can justify adjustments the adjuster’s report missed.

- Ask about missed adjustments: Confirm sales tax, title fees, and any regional market adjustment were included. These are commonly left out unless requested.

- Get an independent appraisal: Many policies include an “appraisal clause” allowing you to hire your own appraiser if you and the insurer can’t agree — costs are often split, and it can be worth it on a meaningful valuation gap.

- Escalate if necessary: If negotiation stalls, most states have a Department of Insurance complaint process, and small claims court remains an option for disputes within its dollar limits.

Frequently Asked Questions

What does ACV mean for a car insurance claim?

Actual Cash Value is what your car was worth right before it was damaged or stolen — replacement cost minus depreciation, based on comparable local sales for the same year, make, model, mileage, and condition. It’s the standard basis for total loss and theft payouts under most auto policies.

Is ACV the same as Kelley Blue Book value?

They’re related but not identical. Kelley Blue Book (and similar guides like NADA/J.D. Power) provide general market value ranges based on broad data. Insurers typically use their own valuation tools (CCC ONE, Mitchell, Audatex) pulling live local comparable listings, which can produce a different — sometimes lower — number than KBB’s published range. Comparing both is a useful sanity check.

Why is my insurer’s ACV offer lower than I expected?

Common reasons include: high mileage relative to the vehicle’s age, a prior accident on the vehicle history report, missed condition credits (recent tires, brakes, maintenance), an outdated or too-narrow set of comparable vehicles, or simply a soft local resale market. Request the full valuation report and compare it against real listings for similar vehicles before accepting — see the dispute section above.

Do I still owe money on my car loan if it’s totaled?

If your loan balance exceeds the ACV payout — common early in a loan term or with a low or no down payment — you’re responsible for the difference unless you have gap insurance, which covers exactly this shortfall. This calculator’s Total Loss Payout tab estimates your insurance payout only; compare it against your actual loan payoff balance separately.

Can I keep my car after it’s declared a total loss?

Usually yes, subject to state rules. The insurer deducts the car’s salvage value from your payout, and the vehicle receives a salvage (or later, rebuilt) title. This significantly limits future resale value and, in many states, requires a safety inspection before it can be legally driven again.

How much does a car depreciate per year?

A common industry rule of thumb: roughly 20% in the first year, then 15% per year through year five, slowing to around 10% per year after that — meaning most vehicles retain only 35–45% of their original value at the 5-year mark. Use the Depreciation Schedule tab above to model this for your specific vehicle and purchase price.

Does low mileage really increase my car’s value that much?

Yes — mileage is one of the most heavily weighted factors after age. A car with significantly below-average mileage for its age (roughly 12,000 miles/year is typical) can be worth meaningfully more than a comparable higher-mileage example, since it signals less mechanical wear and more remaining useful life to a buyer.